What is meant by Price Floor? Discuss in brief, any one consequence of the imposition of floor price above equilibrium price with help of a diagram.

OR

How is the price of a commodity determined in a perfectly competitive market? Explain with help of a diagram.

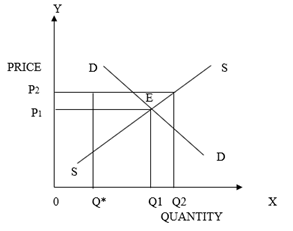

The price floor is the government imposed limit on the minimum price that should be charged for a commodity. The government sets floors or minimum prices for the commodities and services whose prices cannot fall below a minimum prescribed limit. This government-imposed lower limit the price is called the price floor. This is more commonly found in agricultural price support programmes. To be effective it should be higher than the equilibrium price.

The market is at equilibrium at E where price is P1 and quantity is Q1. When the government imposes a price floor that is higher than the equilibrium price P2, the market demand is Q*. But at this price, the firms want to supply the quantity Q2. This creates an excess supply in the market to the quantity Q* Q2. When the market experiences the situation of excess supply, the price of the commodity falls below the equilibrium price. To prevent the price from falling because of the prevailing excess supply, the government will purchase this excess quantity at a pre-determined price. Thus when a price floor is imposed above the equilibrium price, the excess quantity will be automatically wiped out by the government to ensure a proper return to the producers.

OR

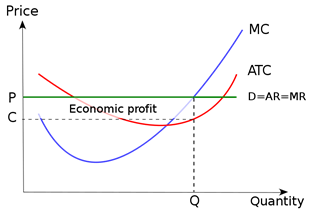

The prices are determined in a perfectly competitive market by the MC-MR equilibrium. It is determined at the point where the marginal revenue equals marginal costs.

Marginal cost (MC) is the change in total cost when an additional unit of output is produced. It is the slope of the total cost curve. Marginal revenue is the net revenue earned by producing an additional unit of output. Under perfect competition, MR will be equal to the price.

TR= P*Q

MR= TR/Q = (P*Q)/Q = P

The prices are determined at the point where profit is maximised under the MC-MR equilibrium. Profit rises when then MR exceeds MC. Losses are incurred when MC exceeds MR. Prices are fixed and profits are maximised at the equilibrium with the fulfilment of two conditions:

• MR=MC

• The slope of MC is greater than the slope of MR i.e. MC curve cuts the MR curve from below.

The ATC curve and the MC curves are U-shaped. This is due to the operation of the law of variable proportion. The D=AR=MR curve is the horizontal straight line MR curve. MR is a straight line under perfect competition as the MR will be equal to price when each unit is sold in the market.

The profit maximising output of the producer is at Q at the point of intersection of MC and MR. At this point, MC=MR and the slope of MC are greater than the slope of MR. At all the levels of output below Q, MR exceeds MC. Thus it will be unproductive for the producer to stop production at this point as this falls under the economically productive region of the producer. Also at all these points, the slope of MR exceeds the slope of MC. But beyond Q, the producer will not produce as it can result in losses. Thus the producer is in equilibrium when the quantity Q is produced at the price of P per unit.

Thus at equilibrium, both MC and MR will be equal. At this point, the prices will be fixed and will ensure the attainment of maximum profits.

Couldn't generate an explanation.

Generated by AI. May contain inaccuracies — always verify with your textbook.